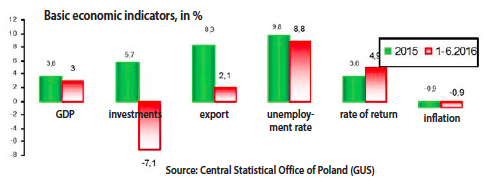

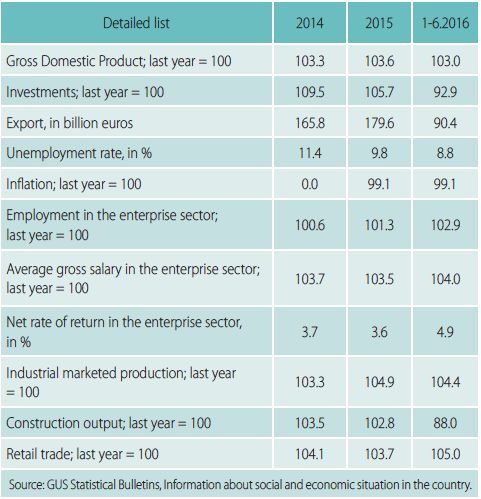

In the first half of 2016 upward tendencies were observed in the majority of economic sectors. Advantageous indicators were recorded in industry and retail sale: industrial marketed production went up by 4.4%, industrial processing increased, and results lower than a year ago were found in mining, power industry and construction. Unemployment declined: the registered unemployment rate amounted to 8.8% in June, which had been the lowest level for 8 years. This June average employment in the enterprise sector was 3.1% higher than last year, and monthly average salary rose by 5.3%. With stable deflation, the purchasing power of salaries increased, i.e. real wages went up. The financial performance of enterprises was better in the first half of 2016 than last year.

However, the beginning of 2016 was characterised by disadvantageous tendencies too: 8.3% more products were exported in 2015 and the exportation in the first half of 2016 (calculated in euro) rose by only 2.1%. After 2 years of higher and higher investments, the financial outlays are clearly dropping. The unstable situation on financial markets is maintained: foreign investors withdraw from the Polish market, fulfilling pre-election promises triggers higher and higher expenditure, and experts voice some reservations concerning the expected revenue budget. Additionally, the consequences of Brexit still remain unknown.

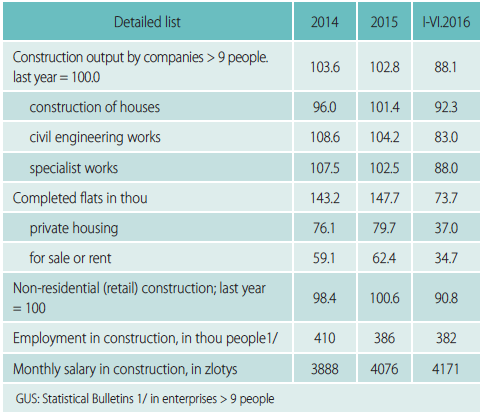

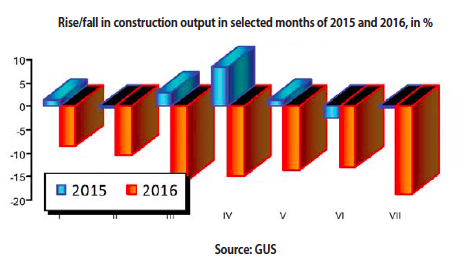

It was expected that the construction industry would combat the recession and take the “path of growth”. Despite the optimistic forecasts, it was a weak and fragile sector of the economy in 2014-2015. Accompanied by strong fluctuations, the output of the construction industry rose by approximately 3%; the renovation construction increased and the investment construction works declined. The first half of 2016 did not bring good news for the industry. Construction and assembly output produced by companies employing more than 9 people was 11.9% lower than last year, and in fact it fell each month of the half of the year. The situation was even worse in public works contracts in the case of which a drop of 1/4 was observed. Hence, a lot of companies are on the brink of bankruptcy.

The analysis of construction indicators by the types of business activity shows that in the first half of 2016 the strongest regression took place in enterprises which mainly deal with civil engineering works. The output generated by enterprises chiefly providing specialist works services was also significantly reduced. A relatively more modest fall was recorded in the case of general construction companies.

Basic indicators in construction

The situation in the construction industry and the development of the sector are mainly influenced by such its constituents as infrastructure, and residential and retail construction. The first half of 2016 was beneficial for residential construction; on the other hand, the non-residential (retail) construction output was lower – fewer hotels and office buildings but more retail and service facilities were erected.

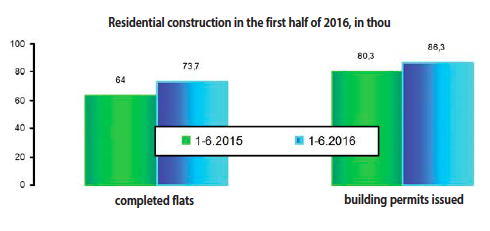

Thanks to the activity of development companies, 73.7 thousand flats were completed between January and June 2016 (15% more than last year). The high pace of constructed flats dropped this July (3.4% fewer dwellings were completed). Poland still experiences a deficit of flats, and, moreover, currently fewer flats are constructed than in 2008. There have been a lot of concepts of residential construction development for the last few years, yet none of them has brought about the expected results. All ideas were focused on assisting buyers in the process of buying the ownership title to flats, and supporting the rental of flats was passed over. The National Scheme of Residential Construction is under formation. One of the main objectives of the scheme is to increase the availability of inexpensive flats for rent. Programme “flat+” (“mieszkanie+”) proposed by the government will be addressed to low-income population. Inexpensive flats for rent at preferential prices are needed and expected, and such a concept should be implemented as soon as possible. But for the time being this is only a slogan. What rises some doubts in particular is the plausibility of the announced very low construction costs of these flats. The low price of a flat in the programme is to derive from a relatively modest standard of dwellings and “free-of-charge” plots from state land resources. Experts already indicate that the possibility of finding plots in built-up areas is slim, and developing plots will increase the costs. There is also another problem: flats for rent should be constructed close to job markets since the location of a flat for rent adjusted to the market demand for employees increases the labour mobilityof those looking for a job.

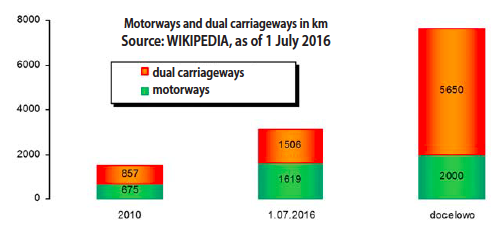

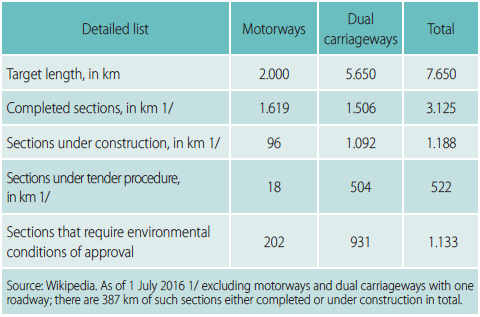

In the case of the infrastructure construction, the preferred area was the construction of motorways and dual carriageways. The scheme, co-financed with UE funds, has been realised for many years, however, unfortunately it has been accompanied by various delays; additionally, the construction costs have also been exceeded. According to the current plans (that have been changed on many occasions) the length of clearways is to eventually reach 7,650 km, comprising 2,000 km of motorways and 5,650 km of dual carriageways. So far (as of 1 July 2016) about 40% of the target has been completed. After the scheme is finished, the length of motorways and dual carriageways (including the completed sections, sections under construction and those for which a tender has been called) will total 4,835 km (nearly 2/3 of the target length).

It is a significant challenge to stabilize the fluctuations in the construction industry. The year 2016 will not make a breakthrough; the construction industry has a chance to attain a substantial rise within a few years though (if no new obstacles appear). However, the delayed tasks in the scope of infrastructure, railroad investments, and expansion and modernisation of the power industry are still to be realised.

Scheme and realisation of motorways and dual

Industry

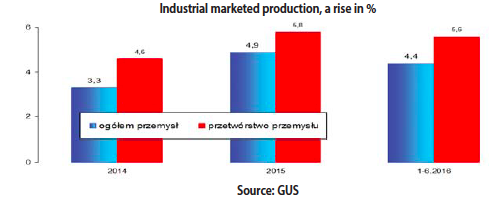

In 2015 the industrial marketed production increased by 4.9%; a stable rise was also maintained in the first half of 2016 (4.4%). The output generated by the mining industry and power industry was lower than last year, but the performance of industrial processing increased. The strongest rise was recorded in the fields that produced a large part of their output for exportation, e.g. manufacturers of furniture, transportation equipment, electrical devices, goods made of metal, domestic appliances, and plastic. Domestic demand for mineral materials used in the construction in the first half of 2016 did not go up, but owing to the exportation of a lot of products the output remained relatively high. The quantity increase in production varied depending on the product type in the first half of the year. The production of materials used for the erection of buildings up to a building shell condition and those not designed for exportation (e.g. bricks, hollow bricks, lightweight concrete blocks, thermal insulation products) was lower than last year, but what increased was the production of some market products and goods designed for exportation (e.g. glassware, tableware and porcelain dishes); the production of components for doors and windows made of plastic and aluminium rose as well.

The beginning of quarter three of 2016 was characterised by falling production (marketed production fell by 3.4%). The majority of lines of business attained poor results: the lowest were recorded in the manufacturing of cars, machines and devices, production of metals, chemicals, electronic tools, and refined petroleum products. It is still too early to assess whether the tendency is of a constant nature, yet it can be seen as a threat for maintaining a good market situation in 2016.

Production of construction materials and glassware

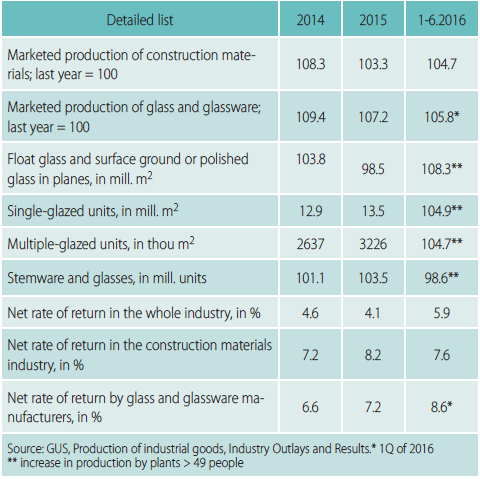

With the diversified tendencies in industrial processing, it must be clearly noted that the glass industry is among the fields with the highest output. Both in 2015 and in the first half of 2016 the production of the glass industry dynamically rose. The share of glass and glassware in the mineral material industry amounted to over 1/4, and was on a slow yet systematic increase. The same can be said about the manufacturing of the most important glassware. Indeed, goods of various materials (e.g. those made of plastic) that have the potential to substitute glass in a number of applications appear on the market, yet glass is material most appreciated by users: especially preferred products are the modern ones made of glass.

The output of cast and rolled glass dropped; on the other hand, the production of float glass, single- and multiple-glazed units, and multilayer safety glass with dimensions and shape adjusted for building in rises.

In the structure of the glass industry the highest share (of about 55%) is made up by profiled flat glass and glass subject to further treatment; traditional cast and rolled glass does not exceed 10%; the share of domestic glassware (glasses, stemware, bottles, tableware or kitchenware) totals over 1/4 of the total output of the industry; the remaining types of glassware are: glass fibre, technical glass, and laboratory glassware for pharmacy.

When assessing the structural changes, one should pay attention to the fact that the rise in the glass and glassware marketed production was higher than the rise in construction mineral materials as a whole; the observation refers to not only the year 2015, but also the first half of 2016 when the value of glass and glassware marketed production went up by 5.8% while the growth rate of mineral materials for construction and market purposes amounted to 4.7%. An important factor influencing the structural changes and ensuring an increase in production is the high share of exportation in the total glass industry marketed production.

The glass industry experiences a strong increase; the financial condition of the sector is good and stable, and the strength of export relations can be perceived as a guarantee against fluctuation on the domestic market.

Both the construction materials industry and the glass industry are fields characterised by a high rate of return. The rate of return in the glass industry has been high for many years (it was 8.6% in the first months of 2016). The main factors influencing the return received by companies producing glass and glassware are the volume and cost-effectiveness of exportation. Additionally, prices on the domestic market and falling costs impact that rate too.

Export

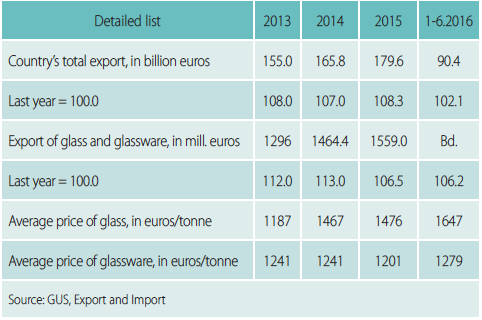

The total Polish export amounted to 179.6 billion euros in 2015, and thus it was 8.3% higher than in the preceding year. The country export to the EU member states was 11% higher, but the export to the Central and Eastern Europe dropped by more than 20%. The most important contractors for Poland in the scope of exportation are Germany (over 1/4 of total export), and Great Britain, the Czech Republic and France (the last three countries together constituted nearly 20% of exportation in 2015). In the first half of 2016 Poland’s export rose by 2.1%; the growth rate of exportation was lower than last year, but more was exported to the countries in the Central and Eastern Europe (a rise of 4.5%). In the product assortment structure a higher than average rise in exportation was observed in the case of furniture, light industry products, ceramic products, products of the chemical industry and pulp and paper industry, and electrical machinery goods. The exportation of farm and food products rose more slowly than on average; drops were recorded among others in the case of the export of metallurgical products and mineral goods.

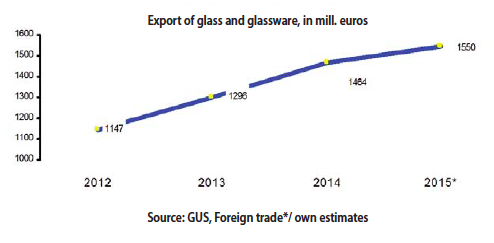

Export in 2013-2016

Poland is still an important exporter of glassware in Europe. In the periods of weak market when domestic demand dropped, enterprises increased their efforts to find foreign markets for their products. The good position of Polish exporters on European markets is a guarantee against any fluctuations on the domestic market. In 2015 the value of exported flat glass and glassware according to initial estimation totalled 1,550 million euros; it was nearly 6% more than in the preceding year. In the first quarter of 2016 the export of glass and glassware in tonnes dropped, but the value of the exported goods increased. Poland is exporting more and more expensive products, which is reflected in a rising average price of exported goods; the price of flat glass went up from 953 euros/tonne in 2012 to 1,480 euros in 2015, and 1,647 euros in the first months of 2016. The price of glassware was stable between 2012 and 2015, with a slight downward tendency recorded in the period, and at the beginning of 2016 it went up to 1,279 euros.

Poland sells to EU member states about 85% of the whole glass industry export. On the other hand, the exportation to the markets of the Central and Eastern Europe is falling. It should be stressed that export strongly impacts the output of the glass industry; the value of exported glass industry products increases more quickly than their production.

Conclusions

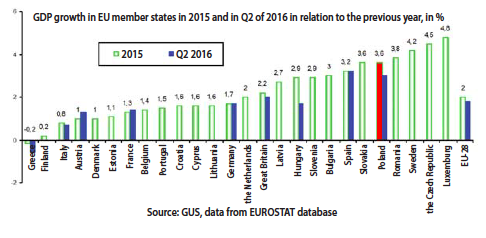

The opinions that the new government found Poland in ruin have not been confirmed. In 2015 the majority of sectors of the economy attained advantageous results. With 3.6% growth in GDP, Poland was among EU member states characterised by the highest GDP growth. Investments rose; despite limitations in the foreign trade with Russia and Ukraine, export exceeded import, and the increasing export improved the recorded industrial results. The financial condition of enterprises was better than in the previous years. Changes in the labour market that began in 2014 started to bear fruit - unemployment decreased. The weakest and least stable sector of the economy was the construction industry, although it is supported with various EU funds.

In the first half of 2016 upward tendencies prevailed in the scope of real economy, but the output was lower than in the previous period; additionally, worrying signals appeared more and more often. The situation on the financial markets remained unstable; exportation was lower, a slump in investments was recorded, which derived from, among others, lower and lower companies’ trust in the stability of the market situation and the withdrawal of foreign investors from the Polish market.

The beginning of this year’s quarter three brought about a reduction in the economic growth rate; the industrial production shrunk; a further drop in construction output was observed and fewer flats were completed. Expectations that the programme called “500+” will result in a rise in consumption and higher retail sales have not been confirmed yet. It is also too early to assess whether the tendencies that took place this July and August will be of a permanent type or not. It is unknown what the effects of the high-spending government policy will be (the policy that realises pre-election promises). The decisions made by the government may have a negative impact on the economy, but their consequences are to take some time to be visible.